Photo: Andrew Parsons.

By Emma Dowling

In September 2014, the G8 Social Investment Taskforce (established by the UK presidency of the G8) produced a report entitled The Invisible Heart of Markets, outlining a strategy for G8 member states to develop a social investment market, invoking the metaphor of the market’s ‘invisible hand’ invoked by the 18th century political economist Adam Smith (1776) in The Wealth of Nations. According to dominant readings of Adam Smith’s theory, it is through the pursuit of one’s self-interest that social activity is steered via a market in beneficial ways for the collective good. The quip in the G8 Social Investment Taskforce report then seems to want to suggest that the market not only has an invisible hand that steers it, it also has an invisible heart that beats for the good of society. In other words, it is not only through the activity of the rational calculating individuals who are intent on maximising utility that people are able to satisfy their material needs such as a roof over their heads or food on the table, but that it is also what might be considered less tangible and more immaterial needs of society that can be satisfied this way: care, sociality, community and so forth. The notion of an Invisible Heart of Markets signals two things: one, that there is an expansion of the market to new areas of social life and two, that while doing so, policy is also responding to the criticisms that arose in the wake of the financial crisis, namely that markets – and in this context specifically – financial markets, have created and exacerbated social ills and negative outcomes. Harking implicitly to the image of ‘greedy’ or ‘selfish’ or ‘excessive’ individuals in the context of the financial crisis, the message here is that financial markets do not have to be dysfunctional, but can be made to work in the interest of everyone and utilised for enhancing social good. Indeed, the report states: “the financial crash of 2008 highlighted the need for a renewed effort to ensure that finance helps build a healthy society. This requires a paradigm shift in capital market thinking from two dimensions to three. By bringing a third dimension – impact – to the 20th century capital market dimensions of risk and return, impact investing has the potential to transform our ability to build a better society for all.” So in other words, by including a consideration not just of financial risk or rate of return on investment, but by including a consideration for the social – and also environmental – impacts of investments and steering investment towards trade that has a social or even ethical purpose, business can be made to produce outcomes that are more consistently beneficial to society. In other words, it would be precisely by going against what Adam Smith is considered to have been suggesting, that financial markets can acquire a heart and produce socially beneficial outcomes. Yet, by invoking Adam Smith, the suggestion seems to be that it is Adam Smith’s purported theory of this invisible steer of the utility-maximising individual that can be extended to ever-more areas of social life and provide a rationale for the benefits of social impact investing. It would seem then, that there is something rather confusing and contradictory going on here with regard to the ways in which financial markets and social benefit are being posited as mutually exclusive on the one hand, and rendered compatible on the other. And it is this confusion that needs working through with regard to the ethical dimensions of new forms of social or impact investing.

What demarcates the social investment market is its distinction from other forms of corporate social responsibility and philanthropy, where the ethical cause is external to the business model. In a social investment market, society is not a separate entity to take from or give back to, but a source of wealth to be harnessed. Hence, ‘venture philanthropy’ is where the social or environmental impact is internal to the ways in which business seeks to create and capture value. ‘Philanthrocapitalism’, as it has been coined, is about “doing well by doing good” in an understanding that investing in projects that are deemed ethical is not only a good thing to do for the benefit of society in general, there is also money to be made in the financial returns on investments that can be generated. Not only that, but social investment market has the potential to mitigate crisis by stimulating the economy. Hence, ‘venture philanthropy’, the argument has it, conveniently offers a ‘win-win’ situation because its forms of social investment also support and augment the kinds of social relations that engender a more ethical, just and environmentally sustainable world.

Social investment is about tapping into both the ethos and the actually existing structures of mutuals, cooperatives, voluntary associations, charities, community groups and so forth. Such organisations offer to venture philanthropy the promise of access to the kinds of volunteer workers or activists who are as innovative as they are imaginative, both at making-do on shoestring budgets and doing good for the sake of it. They can also provide contacts with organisations embedded in existing communities and with the sorts of participatory and grassroots-orientated traditions that are life-blood for social investment. Providing care, running a community library, planting trees in a local area: these kinds of projects speak to many people’s desires to be engaged in meaningful activities. These are the kinds of activities that are also directly related to survival and well-being, the reproduction of life and livelihood. Importantly, the myriad activities that can fall under the rubric of social impact or social value all require those involved to be engaged in building and nurturing social relationships with others. Hitherto what has mattered for neoliberalism has been the individual entrepreneurial drive. With venture philanthropy this is not lost, but what becomes paramount is the activity with others – making connections with others in one’s community, group, project or locality. The onus is on harnessing the social energies of collective action, where this collective sociality is both a means to an end and a very end in itself – the good society.

On the surface of things, this might sound like a good idea – and, if a choice had to be made, who would not rather investors put their money towards good causes than ones that cause harm? Yet, there’s a slippage in meaning here. The slippage lies in the conception of ethics and its relationship to capitalism. The celebration of the social investment market as a novel form of value creation that is socially just in ways it might not have been before relies upon the construction of an opposition between ‘ethics’ and ‘capitalism’. ‘Ethics’ and ‘capitalism’ are depicted as distinct and opposing entities that can be fused together to produce a better world. This is a distinction that plays to the criticism that corporations lack any consideration of values other than the value of profit. The opposition between ethics and capitalism also seems to sit well with the criticism of individuals in the banking sector for their alleged personal greed, dishonesty and short-term profit-orientated thinking that is conventionally put forward as one of the causes of the crisis. Consequently, ethical conduct would constitute the opposite of being greedy or dishonest, or of thinking only of the short-term. Ethical conduct then, is about being mindful of the welfare of others and the wider community, being transparent and thinking not just about a fast buck, but about the longer term. These are all virtues attributed to social investment.

Adam Smith compared the market to an invisible hand. But could philanthropy lend it an “invisible heart”? Photo: Caitriana Nicholson.

There are false polarities being set up here. To suggest that capitalism has now taken, or can take, an ethical turn for the better is to suggest that its earlier form was one that was not ethical. This supposes a distinction between a pre-ethical capitalism and an ethical capitalism, the implication being that capitalism previously only provided things that were simply frivolous or harmful. This is not so: while capitalism as a system has been responsible for suffering and lack, it has also provided for things that people have wanted and needed. The problem is that capitalism only provides if it can do so profitably, and this is done by imposing the commodity form and the wage relation as the way in which people access the means of their reproduction and thereby maintain their livelihood. Capitalism as a system organises production and reproduction in such a way as to enable the private appropriation of the social wealth that is produced, relying on sources of unpaid labour and, as is becoming acutely obvious in the face of climate change, extensive ecological resources to do so. As a social relation, capital is a relationship that is based on unequal power relations founded in an unequal access to or control over the means of social reproduction. What is at stake then is the question of how the material relations of power and wealth that underpin the control over the reproduction of livelihood are organised, maintained and reinforced. Capital is not a subject that can be imbued with a moral agency per se. What matters for the capitalist system is economic value and its augmentation: profit, growth, dividends, returns on investment.

Ethics on the other hand refers to the ways in which people relate to one another and make sense of the relationships between themselves and others; ethics is also normative and prescribes certain forms of sociality. Importantly, ethics is as much a set of ideas as it is a set of practices and relationships. Consequently, a more realistic depiction of what might deserve the term ‘ethical capitalism’ is not the mutually beneficial fusion of ethics with capital as is suggested by the idea of venture philanthropy, but ethics’ subsumption under capital, the rendering profitable of social energies and social practices. Social investment is like any other form of financial investment. Even when ‘ethical’ in its orientation and geared towards a social purpose, it can go nowhere unless it gets a financial return, in the form of dividends or interest for example. And the imposition of a profit motive on social activity not only harnesses, but also disciplines social activity in certain ways conducive to the production of profit.

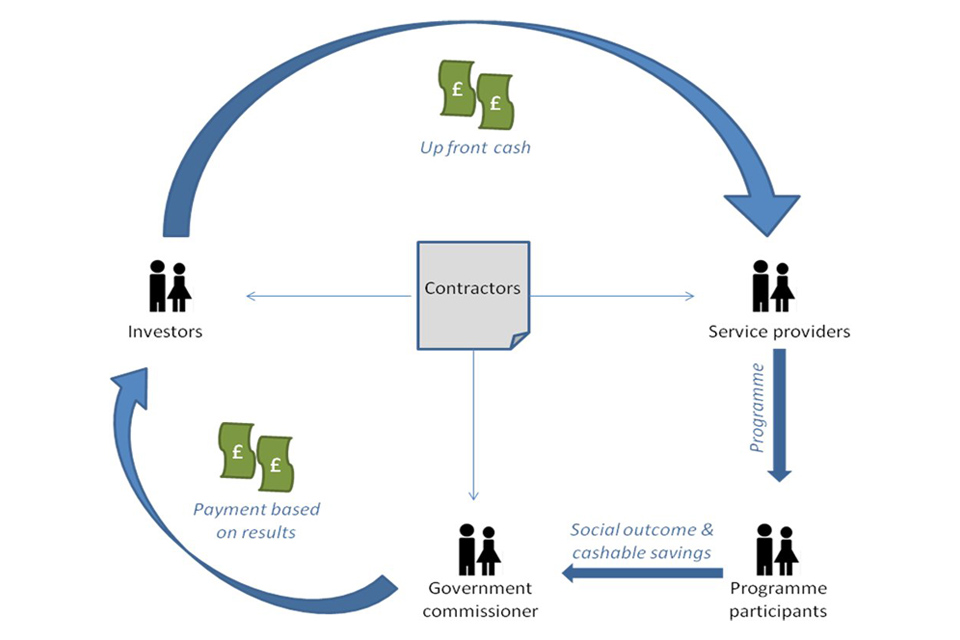

The proverbial devil is in the detail. The appeal to the explicitly social return on investment obfuscates what counts as a financial return and how it is measured. Take for example social impact bonds. A social impact bond yields in the event of a positive social outcome. This means financial returns to investors are made on the basis of achieved targets. If outcomes are not achieved, investors do not recover their investment. To begin with, this begs the question of how social impact targets are set. Clearly, in order to make this work, the targets set have to be quantifiable – they need to be able to be tallied up in units of success or failure, otherwise a rate of return would not be able to be determined. Moreover, benchmarks are required against which the success or failure to meet a target can be ascertained. Money is made by service providers under pressure to meet their targets. Contrary to what it might seem then, the metrics of social return on investment actually hard-wire the drive for investment returns into the process by deploying these as incentives for achieving the end of producing social value.

Social value can include things like addressing climate change through community projects that serve to reduce emissions; social value can also mean improving the attitudes of young and disadvantaged pupils towards their education, or reducing recidivism, or fostering intergenerational exchanges between young and the elderly for the benefit of both parties; social value can also refer to ‘added value’ in existing service provision by involving volunteers from disadvantaged backgrounds or delivering educational activities. Social investment can work across the ‘traditional’ sectors of public services – education, health, eldercare, childcare, housing, social services, but can also involve new projects for social and community development. (See, for example, see the UK Cabinet Office report, The Public Services (Social Value) Act 2012: One Year On).

Graphic: Cabinet Office

Amidst the proliferation of models for measuring social value, there is one model that has become the most dominant and wide spread. What is striking is that this model is one that appears to be particularly useful for linking governments and public services to the social investment market. This is the SROI model, a model of ‘Social Return in Investment’ first tabled by a venture philanthropy fund in the US in the 1990s. Its particular advantage is that it can quantify and ascribe monetary value to social value by calculating cost-efficiency and returns on investment. In other words, it can attach monetary values to social outcomes, but it can also do so in terms of a cost-saving calculus, something that not only businesses care about, but so do governments concerned with reducing public deficit. Consequently, by calculating and demonstrating the amount of social value they can produce, organisations tendering for government contracts compete with one another to provide the service in the most cost-efficient and cost-saving way. The successful tender will be the one who can show that for each £1 invested they can maximise the return on that investment. So, the government can calculate how much it can save for every £1 invested in a social enterprise. One of the ways costs can be saved is to recode inputs (costs) as outputs (social value). The promotion of civic and social activism, the enhancement of community engagement, the fostering of social cohesion become social value outcomes rather than inputs into the labour process, the latter being thereby obscured. If a project fulfills its stipulated aims and produces the designated social value, then the government (i.e. the taxpayer) will pay the investor a financial return on that investment. There are significant political questions here: firstly, with what justification is there a transfer of wealth from the public to the private taking place here and secondly, what constitute desired social values, who decides and how?

But it is not only the qualitative content of social value that is at stake. The development of quantifiable metrics of social outcomes that allow for cross-sector comparison and for pricing outcomes is the first step towards creating a market. Yet, when social value becomes a commodity, it comes full-circle back to qualitative concerns. This is because the precise measure of social value is what gives it its shape, in turn ‘shaping’ social relations that can be subjected to the calculus of financial markets. While an emphasis is placed on the social return of investments in social value, organisations will be required to generate a surplus through trade, government contracts, grants or donations in order to repay investors. (This is outlined by by the financial institution Big Society Capital). Moreover, there is the expectation that social investment markets will operate in the same way, that is with the same kinds of risk and return characteristics as any other kind of financial market, with potential investors including trusts and foundations, mainstream financial investors and high street banks. This also raises the question of secondary markets and their emergence in the face of the fact that financial investors do not always wish to hold financial assets in perpetuity, but also because secondary markets are financial risk management tools. What impact will these secondary markets have on the projects to be financed?

A closer look at the restructuring of public services currently taking place suggests that in the example of the UK, there are attempts to resolve a crisis of social reproduction by simultaneously transferring the cost of social reproduction onto individuals and communities and also by seeking to render these activities and relationships profitable through social investment. In part, these efforts seem to be relying on the unpaid volunteering activities of the population in ways that recode these not as inputs, but as outcomes, i.e. their cost is externalised. They would also not seem to be immune to the vicissitudes of competition imposed by the logic of finance. Moreover, the way that social impact bonds are supposed to work suggests a transfer of more wealth from the public to the private. Therefore, should we not be interrogating the very meaning of ‘investment’ to ask whether ‘investment’ might not actually be a means for disciplining social activities for the purposes of extracting wealth from society rather than making resources available for social purposes and involving citizens in the decision-making on how to do so? Indeed, could this kind of ‘democracy through the market’ ever render a democratic model that is meaningful in practice and worthy of the term?

Dr Emma Dowling is Senior Lecturer in Sociology at Middlesex University and can be contacted at e.dowling@mdx.ac.uk. The text draws on research published in Dowling, E. and Harvie, D. (2014): ‘Harnessing the Social: State, Crisis and (Big) Society’, Sociology 48 (5): 869 – 886. It was presented at the JWI’s Philanthropy and Social Justice Conference in Edinburgh on March 26th 2015.

Dr Emma Dowling is Senior Lecturer in Sociology at Middlesex University and can be contacted at e.dowling@mdx.ac.uk. The text draws on research published in Dowling, E. and Harvie, D. (2014): ‘Harnessing the Social: State, Crisis and (Big) Society’, Sociology 48 (5): 869 – 886. It was presented at the JWI’s Philanthropy and Social Justice Conference in Edinburgh on March 26th 2015.